The Price of War: A Macroeconomic Analysis on the Impact of the Gulf War

By Flavia Lo Giudice | 15th of April, 2026 | 8 min

The 2026 Iran war has led to what the International Energy Agency has characterized as the "largest supply disruption in the history of the global oil market". Since its beginning, the conflict has often echoed the 1970s energy crisis through acute supply shortages, currency volatility, and the looming specter of stagflation.

Firstly, the conflict has introduced a significant risk premium to crude oil prices. While global demand was already softening, the threat to major transit points like the Strait of Hormuz (through which 20% of global oil flows) has caused prices to fluctuate based on geopolitical headlines rather than just supply and demand.

Central banks, which were beginning to signal an end to interest rate hikes, now face a second wave of inflation risks. Higher energy and shipping costs act as a tax on consumption, potentially forcing rates to stay higher for longer to combat rising producer prices.

Secondly, the conflict inserts itself in a global trend toward rearmament, that we have already witnessed since the Russia-Ukraine War. Governments, particularly in Europe and the Middle East, are reallocating budgets toward defense, which often comes at the expense of social spending or green energy transitions: the traditional “guns vs butter” dilemma.

Oil prices dropped significantly following the announcement of a two-week US-Iran ceasefire on April 8, 2026, with Brent crude falling near $95 a barrel. The truce lowered immediate geopolitical risk, calming markets that had previously seen prices surge. However, prices remain elevated above pre-conflict levels, due to fears over the deal's longevity and the seriousness of the commitment of both parties. This is the typical economic “'rockets and feathers” trend: prices rise like rockets but then descend like feathers.

So what are the true economic risks the world would face in the eventuality of a prolonged conflict? Experts talk about a possible economic shock comparable to the one experienced with Covid. S&P warns of a plausible European recession, with Italy to be hardest hit. The conflict, however, risks spreading well beyond energy. The Gulf is a central hub for fertilizers, as well as for strategic raw materials like helium, which is fundamental for high-tech sectors such as semiconductors and healthcare.

According to L. Subran of Allianz, many industries are now facing a Darwinian challenge: rising costs, production disruptions, and a forced selection between more and less resilient firms. This is a pattern already seen during the pandemic, but one with a different origin and potentially more difficult to manage.

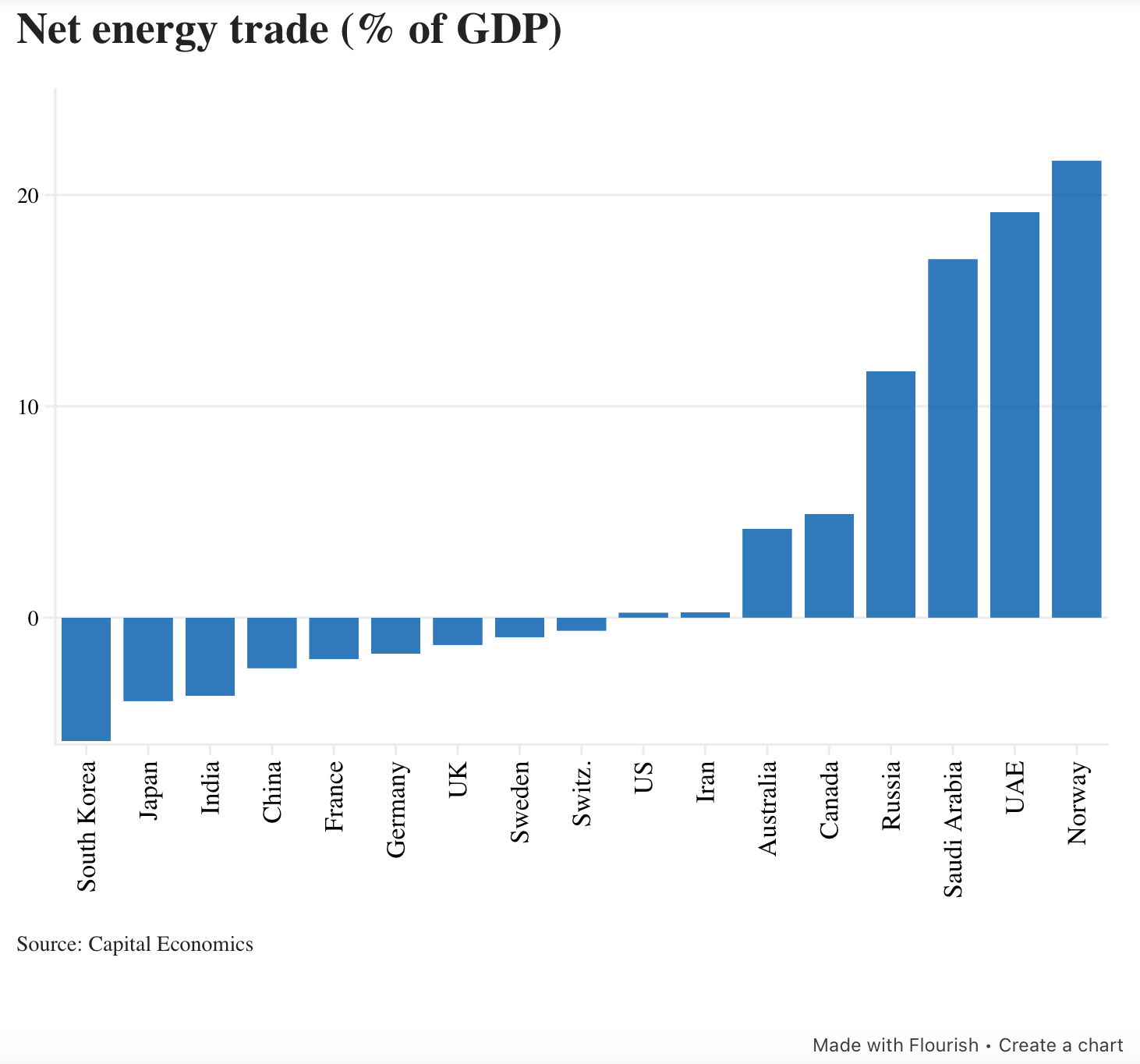

The heaviest burden will inevitably fall on the region itself. History offers a guide: during the 12-day war last summer, Israel’s economy contracted by around 1% in the second quarter. If the conflict is short-lived, a fall in output of a similar order of magnitude would seem plausible for both Israel and the Gulf economies. A more prolonged conflict would almost certainly inflict a deeper economic wound: output would be disrupted, investment postponed and tourism curtailed. Iran’s economy will be hit even harder. Based on the impact of wars elsewhere, GDP is likely to fall by more than 10%. The obvious winners are large net energy exporters outside the Gulf, whose ability to sell abroad is unaffected. Countries such as Norway, Russia and Canada stand to benefit the most from higher energy prices.

The Asian countries are the second most penalized by the current crisis. China, India, Japan, South Korea, and Pakistan have historically been the largest purchasers of gas and oil transiting through the Strait of Hormuz. Consequently, they have now begun a race toward America for supplies. On the other hand, in recent years, they have also secured their positions by increasingly pushing for renewables. This has been the strategy adopted by countries like China and Pakistan, for instance.

The risks for the USA and European countries appear more limited. In fact, only about 4% of the oil transiting through Hormuz is destined for Europe, while the figure for the USA is even lower, with just over 2% of the oil passing through the strait headed for the American market. In short, it is evident that although the conditions for a cascading shock are present, not all involved countries are exposed in the same way. For Europe, in any case, the scale of this shock would probably be smaller than the one following Russia’s full-scale invasion of Ukraine, when it faced an abrupt and dramatic disruption to its energy supplies. The current conflict, unless it escalates dramatically, is unlikely to provoke large-scale fiscal rescue packages from governments.

However, the U.S. and Europe are far from being on the same curve of impact. The United States bears primarily the direct costs of the conflict. Europe, however, risks paying a higher price relative to GDP due to itsenergy dependency. The ECB has already stated this explicitly: the Middle East conflict is being factored into Eurozone projections through lower growth, higher inflation, and less favorable financial conditions. In other words, for Europe, the war is not merely a foreign policy issue: it is a variable capable of altering the cost of capital and, consequently, the competitiveness of its industries.

The overall impact of this disruption to energy supply chains and a sustained increase in oil prices will therefore be asymmetric. Countries like the United States will see inflationary pressures on consumers attenuated by their position as a net energy exporter. Donald Trump is already paying a high price for the decision to proceed with the conflict. However, American citizens are the ones truly paying for the economic consequences. In the U.S., diesel has reached $5.68 per gallon, just below the 2022 price following the outbreak of the war in Ukraine ($5.81). Not to forget that Trump had centered a significant portion of his electoral campaign on this issue, promising to “halve” energy costs. Conversely, countries like China and India, which are heavily dependent on Gulf crude, will have to face consequences for their economies that remain, as of now, unpredictable.

The scale and persistence of the energy shock will ultimately determine its macroeconomic impact. For energy-importing economies, the main transmission channel is likely to be via inflation. Higher oil and gas prices raise the import bill faced by households and firms, squeezing real incomes and eroding purchasing power. Recent signals provide some hope that the conflict may not last long. If so, and provided there is no lasting damage to energy production facilities, the recent spike in oil prices to above $100 per barrel would likely prove temporary, allowing most advanced economies to absorb the shock without significant disruption.

Flavia Lo Giudice is a 2nd-year International Economics and Management student.